Commercial lending 2026: Reasons to be cheerful in commercial property

Publication Date: Friday, 08 May 2026

This article originally appeared in Mortgage Professional Australia

Going with the flow is not an option as rising rates, global shocks, surging migration and tech reshape Australia’s commercial market

“Firm and patient optimism always yields its rewards,” Mexican oligarch and former world’s richest person Carlos Slim once said. A bit of that wisdom wouldn’t go astray for commercial brokers right now.

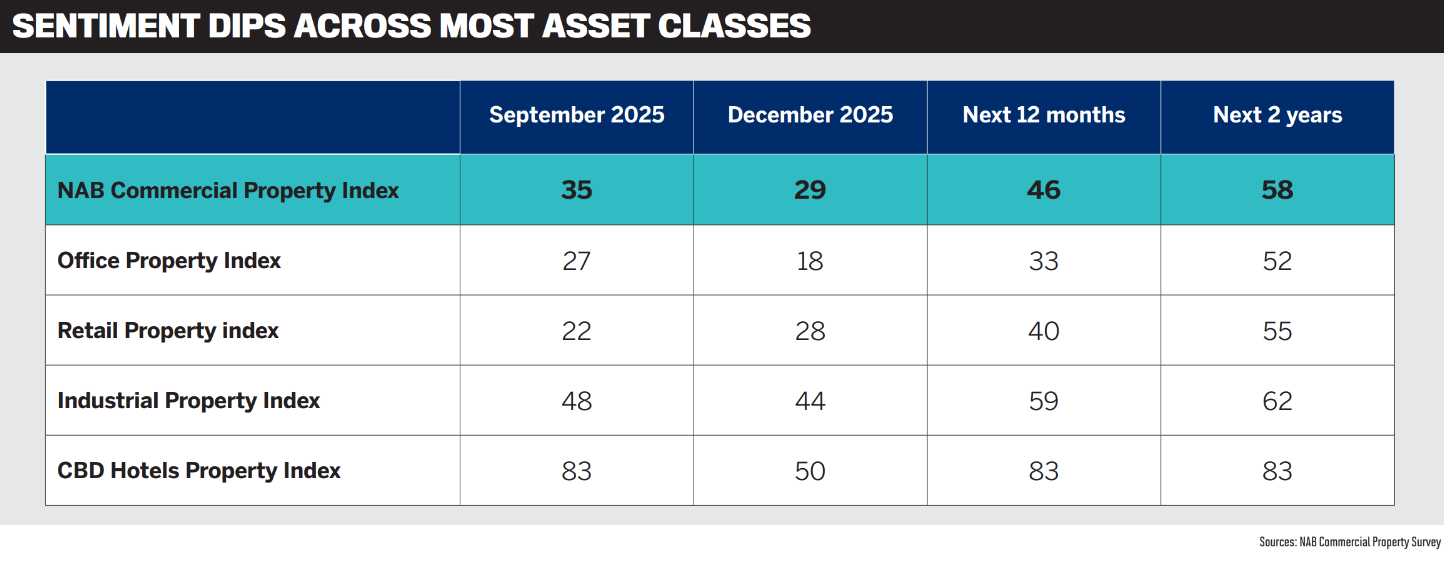

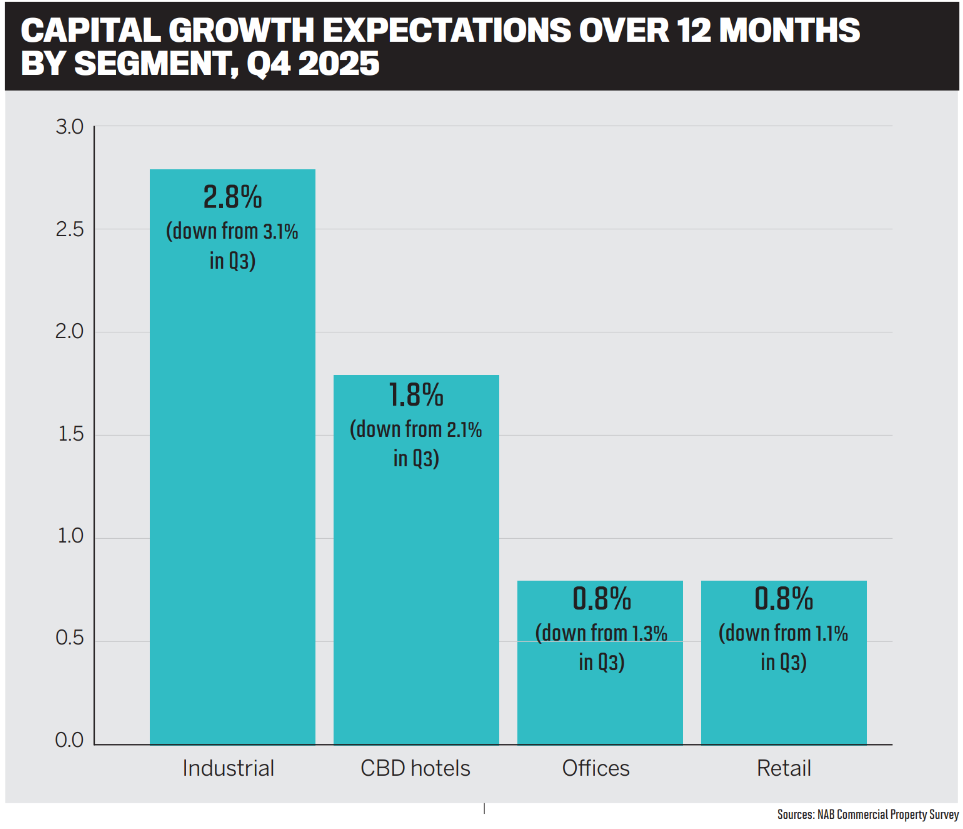

Amid falling business confidence, lower capital growth expectations, high CBD vacancy rates and, of course, a Middle East war that threatens to disrupt all corners of the Australian business environment, few would blame you for being jittery about the commercial property outlook.

Yet across Australia’s diverse business landscape, new opportunities are emerging for commercial brokers within certain sectors, regions and demographics.

Speaking with MPA, industry experts across the banking, non‑bank lending and technology sectors universally acknowledge that the headwinds are real, but so is Australian businesses’ ability to roll with the punches.

Stuck in the middle

“Right now, we believe the commercial property market sits somewhere in the middle,” says Liberty chief distribution officer David Smith (pictured top, left). He notes that the tone is cautious as clients await clarity on how current global events will impact market conditions in the long term.

Chris Thomas (pictured top, right), executive commercial broker and equipment finance sales at NAB, phrases the mood as “tilting cautiously towards optimism”, even as parts of the broader economy “remain uneven”. While business confidence softened in the March quarter, “conditions have broadly held up, sustaining the gains made through 2025”.

Brighten’s head of commercial lending, Ben Mckell (pictured, below), cautions that, with the Reserve Bank of Australia (RBA)’s tightening cycle bringing the rate back up to 4.1% in March, volatility in valuations and borrowing costs is on the rise. Higher rent, medical and insurance costs haven’t helped, while trade‑related volatility “has further weighed on economic confidence and investment planning”.

Mckell doesn’t dance around the issues. “No one expected fuel to be hitting $3.50 a litre, and no one thought a rate rise would come again so soon,” he says. “Inflation is unfortunately out of control, and it creates a cyclical impact; tenants, whether residential or commercial, are going to see their rents significantly increase over the next three to six months or at their next rental review.”

That said, Smith is still seeing businesses investing where it makes sense, all the while relying on experienced brokers “to help them navigate risk and structure deals in a complex environment … While the conversations might be more considered, the activity is still there.”

Thomas is confident that underlying momentum will remain in place, with forward indicators such as capital expenditure plans and orders heading in the right direction.

At ORDE Financial, director of distribution Lee Prior says, “What we’re hearing from brokers is there’s still plenty of movement, especially from SME owners, and that’s a positive sign.” Business owners are being practical with their lending needs: while conditions are far from perfect, they’re working with brokers to get their businesses in the best position available to them. This can range from buying their premises outright to lock in certainty, to refinancing or restructuring debt to optimise cash flow.

But “it’s certainly not a boom”, adds Craig Stuart (pictured top, centre), head of commercial at MA Money, “and performance across commercial assets remains highly dependent on asset quality and sector dynamics. The biggest headwinds are likely linked to broader economic uncertainty, particularly given ongoing global events. The impact of Middle East tensions means we’re seeing upward pressure on inflation, leading to cash rate increases and localised rate increases.”

Australia’s industrial powerhouse

The industrial property segment – including warehouses, workshops and mixed‑use properties – seems to be a hive of activity in 2026, thanks to a combination of limited stock and strong demand that has driven price appreciation.

NAB data shows that industrial continues to outperform on sentiment, capital growth and rental expectations, due to low vacancy rates and ongoing demand linked to logistics, warehousing and supply chain resilience. “That’s translating into sustained borrower confidence and a steady pipeline of high‑quality deals,” says Thomas.

At MA Money, over 35% of enquiries are currently geared towards the industrial segment, fuelled by growth across e‑commerce, logistics and manufacturing. “Tenant demand appears to remain high in many markets and in some cases is outstripping supply,” says Stuart. He is seeing strong appetite for vacant land in growth regions on the fringes of metropolitan areas.

Outside of industrial, Mckell has witnessed a renewed interest in some specialist commercial property assets. “We have seen quite a few examples of just your normal residential property investor looking at diversifying and buying boarding houses, which fall in that commercial realm,” he says. Additionally, childcare centres are being seen as an attractive asset class with good rental yield.

‘Silo warehouses’ are gaining traction as a hybrid solution for online businesses, combining storage, light industrial and flexible workspace in one. “Unlike residential, there is still a good supply for commercial assets, hence it represents great opportunities for investors diversifying into the space,” says Mckell.

While office spaces remain in a post‑COVID slump, with vacancy rates still higher than expected, there is “selective interest in retail and office assets, particularly in locations with strong tenant profiles”, says Smith. “Where the fundamentals are good, confidence tends to follow. Brokers who really understand their local markets will be finding solid opportunities.”

Migration redrawing the commercial map

Through ORDE’s work with demographer Bernard Salt, the lender has zeroed in on how migration is reshaping the commercial property market across the country.

Research shows that around 32% of Australians were born overseas and, in many outer‑metro and regional corridors, migrant communities aren’t just settling. “They’re starting and growing businesses, which naturally drives demand for commercial property like workshops, warehouses, office and clinic suites and mixed‑use sites tied directly to the business,” says Prior.

This shift is most evident across the country’s commercial heartlands in the eastern seaboard cities of Brisbane, Melbourne and Sydney, where new employment precincts and SME clusters are forming alongside population growth.

Prior (pictured, below) says “investment across Australia’s commercial heartlands remains strong, underpinning business confidence, job creation and the growth of new precincts and communities”.

ORDE’s data shows that commercial and industrial building approvals are up around 27% compared to pre‑pandemic levels. “[This] tells us businesses are still planning and investing,” says Prior. “And when you look at segments like tradies (a big driver of SME activity), the numbers continue to grow, with close to two million tradies nationwide, many of them running their own businesses.”

For brokers, those trends translate directly into commercial opportunities as business owners move from renting to owning, while upgrading to more suitable premises or bringing property into SMSFs.

“These are also the areas where brokers are most active,” Prior says. “Our role as a non‑bank is to back brokers in those moments with lending solutions that reflect how these businesses operate. From our perspective, understanding how these shifts play out business by business is what ultimately drives commercial property loan activity.”

Tech‑driven broker growth

As brokers capture an ever‑greater share of the commercial property market, technology is becoming fundamental to their growth.

Systems like NextGen’s ApplyOnline platform, the standard bearer of Australian loan application and lodgement, play a pivotal role in driving this expansion. NextGen chief customer officer Tony Carn says, “NextGen’s role is fundamentally about removing the friction that has historically made commercial lending feel out of reach for brokers who’ve built their practice around residential.”

ApplyOnline is already ubiquitous in the Australian broking industry, which means most brokers can manage commercial applications on a platform they’re already familiar with.

“Importantly, as brokers work through commercial applications on the platform, the structured workflows and lender‑specific requirements built into ApplyOnline actively help them understand how commercial loans are put together – so the platform itself becomes part of the learning curve,” says Carn.

ApplyOnline supports brokers by outlining each lender’s policies and requirements while offering dynamic checklists that change from deal to deal and lender to lender.

But tech can only take brokers so far. Commercial lending is inherently more complex, and involves considerably more variables, than residential lending.

Carn regularly sees brokers approaching commercial applications with a similar mindset to residential lending, which can frustrate and delay the loan application process. This underscores the importance of user‑friendly systems and portals at the lender level.

“[Brokers’] demands haven’t just changed; they’ve crystallised,” Carn explains. “Commercial brokers now expect the same guided, structured lodgement experience they have for residential, and lenders are increasingly recognising that providing that experience is a competitive advantage in attracting broker business.”

Thomas attests to this. Brokers’ expectations of their lending partners continue to rise, “and rightly so”, he says. “Today’s commercial brokers are looking for faster clarity, greater flexibility and deeper relationships with their lending partners – not just sharper pricing.”

Brokers are looking for early, informed conversations that quickly surface whether a deal is feasible, so they can manage client expectations with confidence. They also value lenders who can tailor solutions around a customer’s broader goals, rather than taking a one‑size‑fits‑all approach.

NAB is meeting these demands “by leaning into our relationship‑led model”, says Thomas. He explains how bankers retain lending authorities, enabling real‑time credit discussions and faster decision‑making. NextGen plays its part by working with its lender partners to build out commercial‑specific configurations within ApplyOnline “so that the platform does more of the heavy lifting in guiding brokers through what each lender actually needs, at the point of submission”.

Open banking is also becoming increasingly relevant to the commercial lending conversation, “particularly for the self‑employed and small business borrowers that commercial brokers typically work with”, notes Carn.

Systems like Frollo, which is owned by NextGen and integrated with ApplyOnline, allow brokers to collect data straight from banks, which reduces the risk of AI‑altered or fraudulent documents. It also removes the back and forth of manual document collection that slows down the application process and frustrates clients.

“For business borrowers, having transaction data that accurately reflects cash flow and income patterns – rather than relying solely on what can be captured in tax returns – can make a genuine difference to both the speed and the outcome of a credit decision,” says Carn. “That’s a real value‑add a broker can offer their commercial clients.”

A matter of complexity

From banks to non‑banks and tech providers, all commercial property experts agree on one thing: the sector represents a massive opportunity for brokers.

Current estimates put broker share of the broader commercial lending space somewhere between 30% and 40% (unlike residential, there is no cold, hard data), but the only way is up.

Mckell estimates that the share has risen from the upper 20% range just two years ago to the mid 30% range today and is expected to hit 50% over the next two to five years.

“Brokers are becoming increasingly confident in the commercial lending space, and we’re seeing a noticeable shift in mindset,” says Mckell. If anything, Brighten’s substantial growth over the past 24 months, expanding its distribution team from six to 20, with dedicated commercial BDMs in Victoria – and New South Wales and Queensland soon to follow – proves that brokers are increasingly influencing the commercial landscape.

Stuart believes education plays a big role in advancing brokers’ influence in the commercial space, with industry bodies the MFAA and FBAA performing “excellent work” in educating and training brokers on commercial property opportunities.

“Combine the fact brokers are looking for more strings to their bow, multiplied by clients having more confidence in the broker market to help with their business and commercial needs, naturally we can expect greater participation,” predicts Stuart.

“We expect more mortgage brokers to step into commercial lending by drawing on the relationships they already have,” adds Smith. “It often starts with a simple conversation about future plans, such as moving into self‑employment or expanding operations. It’s all about asking the right questions. Liberty works closely with brokers to build their knowledge and confidence so they can identify these commercial opportunities and workshop scenarios with us.”

As uncertainty around growth, inflation and interest rates has increased, “brokers have become more central to helping customers navigate trade‑offs between timing, structure and risk, and are increasingly supporting customers to plan for a wider range of potential outcomes”, says Thomas. He is seeing brokers move beyond transaction execution into a more advisory, end‑to‑end role by supporting clients earlier in the journey, shaping funding strategies and helping customers weigh up risk, timing and structure.

“At the same time, the quality of brokers entering commercial lending has lifted,” says Thomas. “More experienced professionals are stepping into the space, raising the standard of deal preparation and customer engagement.”

“Commercial lending isn’t new, but the opportunity for brokers has never been clearer,” continues Prior, who describes a holistic approach to growth.

“Commercial property decisions today are rarely standalone. They sit alongside broader business and personal considerations for the client, which is why brokers who stay close to their clients – and build strong working relationships with accountants, advisers and other intermediaries – tend to create deeper, longer‑term opportunities as needs evolve … Brokers are far more central to these conversations now.”

Despite the increasingly diverse needs of borrowers, Smith says it’s a common misconception that commercial loans are too complex. “While some applications do require more detail, many are more straightforward than brokers expect … With the right support, brokers can start to see possibilities in the commercial space, rather than challenges, which in turn strengthens their own offering to their clients,” he says.

Prior believes complexity often comes from business owners’ “layered financial situations”. He explains, “They might have strong turnover and solid businesses but also ATO debt, legacy lending structures or short‑term facilities that were put in place during tougher periods and no longer make sense.”

While that can look risky, “in reality, it often just needs the right structure and the right lender”, says Prior. He notes that commercial lending has been central to ORDE’s growth over the six years since it opened its doors. Today around 80% of ORDE’s book supports SME owners and operators. “This isn’t niche or fringe lending. These are everyday business owners who keep the economy moving – employing people, investing locally and adapting as conditions change.”

As a relatively new player in the commercial world, MA Money is “mindful that awareness is paramount”, says Stuart. To build awareness, MA Money has recruited a national BDM team to meet brokers where they operate. Simplicity is the name of the game at MA Money. “Our commercial product range shares similarities with our residential product suite, ensuring a more simplistic approach that most brokers can resonate with. The aim is to not overcomplicate the process,” says Stuart.

Brighten, meanwhile, is meeting broker demands “by continuing to invest heavily in our people, our processes and the way we support brokers”, says Mckell. “Brokers value responsiveness and clear scenario guidance, so we have expanded our team to ensure we can respond quickly and provide meaningful support at every stage of a deal. We are also simplifying our internal.”

NAB is also investing heavily in broker capability, education and support – from credit skills workshops to dedicated banker coverage across Australia – so brokers know exactly who they’re dealing with and where to go for help. In 2025 alone, NAB delivered 29 commercial credit skills workshops to around 650 brokers, alongside a further 10 bespoke sessions tailored to key aggregator partners. “The focus is simple: reduce friction, improve certainty and support brokers to deliver better outcomes for their customers,” says Thomas.

An uncertain outlook

There remain some pretty sizeable question marks hanging over the commercial property outlook. Despite well‑documented resilience among Australia’s small business community, there’s no way of knowing how the ripple effects of the Iran war will play out.

Energy shortages are a pervasive threat that risk causing price shocks in all corners of the Australian economy – commercial property included. If the most hawkish of RBA rate predictions play out, alongside persistent supply chain pressure, there could be challenging times ahead.

“We are watching global political developments closely and considering how they may impact financial markets, inflation and energy prices,” says Smith. “Shifts in these areas typically flow directly through to commercial confidence. For brokers, understanding how customer needs change in this environment will be key. The more tailored the solution, the better the outcome could be for the borrower.”

For now, uncertainty reigns. As Mckell explains, “When we look at market interest at the moment, it really is hard to predict. Locally in Australia, the current mood is shaped by the fuel crisis, the rising cost of living and rising interest rates, along with what’s happening overseas.”

Stuart also cautions that tighter disposal income among Australian households “could lead to softer consumer spending and potentially temper momentum in certain sectors”.

But this uncertain economic climate only serves to reinforce the importance of brokers in delivering personalised solutions for business owners.

As Prior says, “SME owners need support across property, debt and growth, and brokers who understand different borrowing structures – and work with lenders that can accommodate them – are well placed to support clients as their needs evolve.”

Is it business as usual right now? Perhaps not, but nor is it as bleak as the news cycle would have you believe.